My newsletter helps immigrants understand the US financial system and puts you on the path to become a multi-millionaire. Fulfill your money dreams with Financial Planning for Millennial and Gen Z immigrants (H1B, L1, Green Card)

Secret to getting rich? All you need is 20 stocks

|

Hi Reader , I know, I know, I’ve been MIA for a while, but you know how chaotic life gets sometimes. Speaking of chaos, are any of you fans of the hindi “Housefull” franchise? No? Okay, how about Spider-Man 3? Why am I speaking about films in a finance newsletter? Well, for those of you who are familiar with these, you know the crazy that ensues in both films because of too many characters? In different ways—Housefull’s plot hinges on too many people in the house who wreak complete havoc and Spider-Man 3 has been criticized for being laden with too many villains, love interests and subplots, eventually diluting a film that could’ve been fun. Your investment portfolio works something like this too. Recently, I had some folks chat me up about a little advice on investing. One look at their portfolio with about 400 different positions (just short of 100 stocks compared to the S&P 500) in a myriad of stocks had my head reeling. Who in their right mind has enough time to monitor so many freaking stocks? But I get it, they were perhaps hoping that investing in specific companies would give them more bang for their buck, maybe even outperform the S&P. But if you really think about it, owning so many positions often ends up with your investment being poorly sized—some positions are just ~0.03% of the total portfolio. Even if one of those positions gave you whooper returns, say tripling overnight, it would still be less than 1% of your invested sum. Now, how’s that gonna get you rich, buddy? Okay, need a little more math to be convinced? Crunch, Crunch, CrunchLet’s say you have holdings (the money you have invested) of $10,000. Any allocation or investment lower than 5% would be at just $500. Say you got that in a bumper stock which doubles, i.e., appreciates 100% in a year, you would still be at net $1,000 on that position, optimistically speaking. Now say the rest of your portfolio gave you average returns of ~10%. Let’s calculate where you’d be at the end of the year:

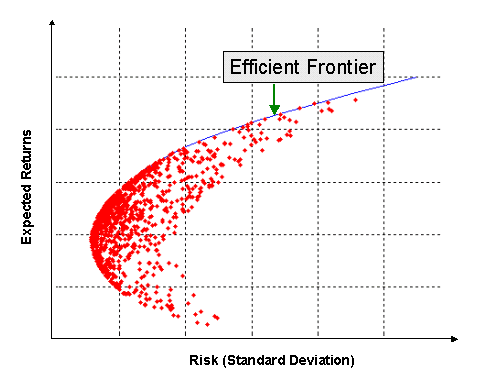

Add these up and you would be at $11,450. Good? Sure. Great? Not really. Let me tell you why. Now assume you had netted 10% on the whole portfolio of $10,000 by investing in a broad market fund. You would be at $11,000 ($10,000 + $1,000). In essence, you’re just $450 ahead because of your “bumper” stock. But do you know how difficult it is to find one that outperforms the market like this EVERY year? You’d either have to be very endowed in the luck department or skill department, and if you had the latter, you would’ve chosen to be a fund manager, no? (In this context, I’m referring to the stock market, where the shares of public companies are bought and sold. As a whole, the general direction of the market, good or bad, will impact your portfolio. There may be anomalies, but largely, most stocks will follow the market trend.) Now what? Let’s Get Efficient!…and also a little technical. I’ll try to make it fun, promise! There’s a concept in finance called the efficient frontier. It represents the best possible (optimal) portfolio of investments that straddle the sweet spot of highest expected returns for the least amount of risk you can take for it.

Source: MarketXLS The optimal portfolio on the efficient frontier are the best investment choices that can give you the highest returns for the risk you’re willing to assume. Sub-optimal portfolios that lie below the efficient frontier will have lower expected returns for the same level or even higher amount of risk. What if you go above or to the right of the efficient frontier? There’s a small chance you can get higher expected returns but is the risk really worth it? Since I promised some fun, Imma explain this with a dessert analogy. (I’m hungry and trying to reason why I shouldn’t eat a whole chocolate cake rn.) Think of the efficient frontier as a beautiful, decadent dessert table at a wedding…when you’re on a diet. Bummer. While loading on three slices of tiramisu can seem tempting for its satisfaction (returns), it will throw the calorie count (risk) way off balance. And an apple or kiwi slice will just not cut it now, will it (low risk, low return)? So, if you’re smart, you’ll curate a plate that’s a mix of everything good in all the right ways—some fruit, some danish croissant, and some tiramisu (and strawberry cheesecake?) without derailing your diet too much. But, you can skip that bland muffin laden with calories, no? Maximum yum for minimum guilt. Approach your investment portfolio like a savvy dessert connoisseur who balances their cravings with their calorie budget. Aha! Honestly, just 20 stocks in your investment portfolio can do the trick. And that also is a bit much, tbh. Frank Reilly and Keith Brown, in their book Investment Analysis and Portfolio Management, outlined a set of studies for randomly selected stocks, noting “…about 90% of the maximum benefit of diversification was derived from portfolios of 12 to 18 stocks.” To paraphrase, if you own 12 to 18 stocks, you get more than 90% of the benefits of diversification, assuming you own an equally weighted portfolio (all assets have equal investment, for eg. you invest $6,666 each in 15 different stocks). But alas, (everything has a but no?) in investing, a grossly disproportionate portion of the total return comes from a very few “superstocks” which outperform the index. By owning only 15 stocks, even one of which is a superstock, you increase your chances of becoming fabulously rich. If you don’t have one of these in your portfolio, then you lose out, badly lagging the market. It is all too often true that the same things that maximize your chances of getting rich also maximize your chances of getting poor. Such is life (which is why you are better off owning the entire market/ buying an index fund) Thoughts?All I’d like to say is in the guise of creating a diversified portfolio, don’t accidentally create a mutual fund. Leave that to the experts. Play smart on your journey to getting rich. Takeaway: If you’re gunning for steady, consistent numbers that outperform an index like the S&P, you need a smartly concentrated portfolio (remember 20 stocks?), but you’ve got to be okay with periods of underperformance too. Alternatively, you could try a hybrid approach for balance. As per usual, if any part of this newsletter tickled your fancy (tiramisu? investment gyaan? More analogies and jokes?), drop me a line! That’s all for today. See you next month! Fun Corners of the Internet

Whenever you're ready, here are 2 ways I can help you:

|

Hi! I'm Vrishin.

My newsletter helps immigrants understand the US financial system and puts you on the path to become a multi-millionaire. Fulfill your money dreams with Financial Planning for Millennial and Gen Z immigrants (H1B, L1, Green Card)

Hi Reader , How are you gearing up for the end of 2024? I hope it’s a merry Christmas for you and your loved ones and that you have time off to recharge, rejuvenate, and plan for another revolution around the Sun. This is also a period when many folks are reflecting on the year gone by, and making new-year goals–health, financial, emotional, and professional. So I come bearing a warning sign of all the financial advice/shortcuts/ courses you might encounter floating on the internet as a...

Dearest Reader, I was at a Diwali potluck at a friend’s house a few days ago. Picture jasmine-scented candles, marigold garlands, a makeshift mandir, bright-colored clothing, game cards, and a table of sumptuous ghee-laden food (which I love, occasionally). That’s not all there was. The living room also had a corner table for gifts—occupied by a tower of 10 sweet boxes (mostly Soan Papdi) piling up atop one another. After everyone had their share of beer, we joked about the sweets,...

Dearest Reader, Let me just come out and say it: networking is a pain in the butt. However, doing it outdoors, someplace like the beautiful Huntington Beach in California, makes it a lot more bearable. So, I attended the FutureProof Festival this year again, and it was every bit refreshing! Look at me beaming in the gorgeous, scorching sun! Of course, I returned with a nice tan and a bunch of new learnings. At the Future Proof Festival 2024 Now, onto the serious stuff! As a financial advisor,...